How To Register Rental Property With State Of Maine

Last Updated on December half-dozen, 2021 past Mark Ferguson

Many people want to purchase investment properties because of the fantastic returns they can provide. Even so, many people exercise not accept the 20 percent downwards payment (or more) that virtually banks require. There are ways to buy an investment property with little coin down. The easiest mode to purchase an investment property with less than 20 percent down is to buy as an owner-occupant and after rent out the house, but there are many other options for investors as well. Using a line of credit, refinancing your home, house hacking, the BRRRR method, or even credit cards can provide ways to buy investment backdrop for less money. Seller financing is a peachy way to put less coin down on a rental property if yous can notice sellers who are willing. A more avant-garde technique is to use hard-coin financing that you can refinance into a conventional loan. Whatsoever way you choose to buy a rental property, research the method to make sure that information technology is legal in your land, your lender approves it, and that y'all are not stretching your finances as well thin.

Many people want to purchase investment properties because of the fantastic returns they can provide. Even so, many people exercise not accept the 20 percent downwards payment (or more) that virtually banks require. There are ways to buy an investment property with little coin down. The easiest mode to purchase an investment property with less than 20 percent down is to buy as an owner-occupant and after rent out the house, but there are many other options for investors as well. Using a line of credit, refinancing your home, house hacking, the BRRRR method, or even credit cards can provide ways to buy investment backdrop for less money. Seller financing is a peachy way to put less coin down on a rental property if yous can notice sellers who are willing. A more avant-garde technique is to use hard-coin financing that you can refinance into a conventional loan. Whatsoever way you choose to buy a rental property, research the method to make sure that information technology is legal in your land, your lender approves it, and that y'all are not stretching your finances as well thin.

How much money down practice most banks crave?

An investor will have to put downward at least xx percent to purchase a property from a typical banking concern. If you ain more than four backdrop, that figure can increase to 25 percent down, providing that they are even willing to finance more than 4 properties. On top of the down payment, an investor will have to pay closing costs, which can range from two to four per centum of the loan amount. It is very expensive to buy an investment belongings using financing from a typical bank. I have constitute a bully portfolio lender who will finance as many properties as I want with twenty percent downward, just they are not like shooting fish in a barrel to find. Once you factor in repairs, carrying costs, down payment, and endmost costs it tin cost as much as $thirty,000 to purchase a $100,000 rental property.

The video below goes over ways to buy with piddling money down as well:

How to buy as an owner-occupant

The easiest way to buy an investment property with piddling money down is to purchase as an owner-occupant, satisfy your loan requirements, rent out the property, and keep it every bit an investment. Almost possessor-occupant loans require the buyer to occupy the home for at least a year. Once that yr is up, you can hire out the house and turn it into an investment belongings. There are many owner-occupied loans available, with down payments ranging from 0 to 5 percent down. Yous can put as much coin down as you desire if you desire to put twenty percent down or even 50 percent down. USDA and VA take great no-coin-downwardly programs and piddling to no mortgage insurance, which will save an investor a lot of money each month. You will have more costs with little money down loans because mortgage insurance is required. Mortgage insurance can add hundreds of dollars to your firm payment and swallow abroad at your cash flow. The process of buying equally an owner-occupant and and then turning the house into an investment property is equally follows:

one. Purchase a house every bit an possessor occupant, which volition greenbacks menses when you rent it out.

2. Move into the house and alive there for at to the lowest degree a year.

- Later on the year is up, find another firm that will cash flow and purchase that dwelling house every bit an possessor-occupant.

4. Move out of the kickoff firm and keep it as a rental. Move into the new house and repeat the process every twelvemonth!

Somewhen, yous will exist building up equity and extra cash flow, which will enable y'all to purchase backdrop with a 20 percent down payment. Repeating this process 10 times would be an excellent way to get started, but no 1 wants to move ten times in ten years. Information technology can besides be tough to convince your family to live in a abode that would be a great rental.

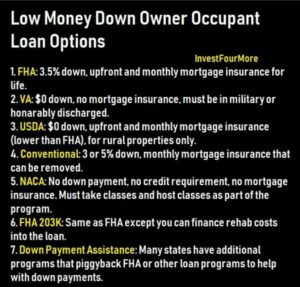

Low down payment owner occupant loans

If you are going the owner-occupant route there are many loans available that have from very little to nothing down required.

FHA loan

FHA loans are government-insured loans that tin can be obtained with as piffling as 3.5 per centum downwardly. Yous tin can only have one FHA loan at a time unless you accept extenuating circumstances like a job relocation. You practice take to pay mortgage insurance on FHA loans, which I will discuss later in this commodity. There are limits to the amount an FHA mortgage can be, which varies by land and fifty-fifty city.

USDA loan

USDA is a loan that tin can be used in rural areas and pocket-size towns. The loan can't be used in medium-sized towns or large towns/metro areas. The loan is a fantastic loan for those that authorize and want to buy a domicile in the designated areas. USDA loans can be had with no money down, but do take mortgage insurance also.

VA loans

VA loans are run through the United States Veterans Administration. You lot have to exist a veteran to qualify for the loan, but they likewise can be had with no money down and no mortgage insurance! VA is a not bad option for those that qualify because the costs are and so much less without mortgage insurance.

Downwards payment assistance programs

Many states take downwardly payment assist programs. In Colorado, nosotros have a programme called CHFA. The program helps buyers get into owner-occupied homes with very piddling money downwards. CHFA really uses an FHA loan but allows for less than a three.5 percent down payment. Check with lenders on your state to see if you lot take any programs that help with downward payment aid.

Conventional mortgages

Fifty-fifty conventional mortgages take depression down payment loans available for possessor-occupants. For owner-occupants, conventional loans have downward payments as low as 3 per centum. You will most certainly have to pay mortgage insurance with whatever conventional loan that has less than 20 percent downward. Unlike some of the other loan options available, y'all tin can take equally many conventional mortgages in your name equally you want every bit an owner occupant.

FHA 203K Rehab loan

An FHA 203K rehab loan allows the borrower to finance the house they are buying and repairs they would like to complete afterward closing. This is a great loan for homes that demand work, but the buyer has limited funds to repair a home. At that place are more costs associated with this loan upfront because ii appraisals are needed and lenders have higher fees for 203K loans.

NACA Loans

NACA is a not-profit program with:

- No down payment

- No endmost costs

- No points or fees

- No credit score consideration

- Below market thirty-year and 15-year fixed-rate loans

This sounds similar information technology is too good to be true, and it is a nifty program. However, y'all exercise not simply apply for the loan and hope the lender approves y'all. Yous must take classes, and even host classes when in the loan program.

More details are on the NACA site.

What loan costs does a buyer demand to consider besides the down payment?

On well-nigh whatsoever loan you volition have more costs than only the downward payment. The lender will accuse an origination fee, appraisal fee, prepaid interest, prepaid insurance and possibly prepaid mortgage insurance. Plus you may take more than costs the title company charges similar a closing fee, recording fees, and possibly title insurance. In most cases, the seller pays for championship insurance, but with HUD and VA foreclosures the heir-apparent has to pay for title insurance. These costs can add up to some other iii.5 percent of the mortgage amount or sometimes more. When you lot talk to a lender they tin can give y'all an estimate of exactly how much these costs will be before you become your loan.

Can you enquire the seller to pay closing costs?

Even though the lenders and title company volition charge y'all more fees than just the down payment, that does not hateful you have to pay that upfront. You tin enquire the seller to pay closing costs for yous. If you tin can get the seller to pay your endmost costs for you, loans similar VA and USDA may be obtained with no out-of-pocket greenbacks. Y'all may still have to put down an hostage money deposit, merely that can be refunded at endmost in some cases. When you ask the seller to pay endmost costs, information technology reduces the amount of coin they are getting from the sale and so you might actually be paying more for the domicile than if you didn't inquire for closing costs. Simply in my heed paying a little more for the house and financing those costs to save cash is meliorate than paying more coin out-of-pocket for a little cheaper domicile.

House Hacking

House hacking is when you purchase equally an owner-occupant only yous buy a multifamily property instead of a firm. By purchasing a multifamily property you can alive in ane unit of measurement while you rent out the other units. This strategy allows you to rent the property faster, which may hateful the bank volition be more willing to give you a new loan as presently as you are ready to motion out. You will also accept assist from the other tenants to pay your mortgage. In some cases, yous may be able to alive for free while you own the house because the other rent covers your costs.

Virtual real manor

Aye, you tin can now buy virtual real manor! This is land in the metaverse that simply exists digitally. Some pieces of virtual real manor have sold for millions of dollars and others tin can be bought for almost nothing. Hither is some more data on getting started!

BRRRR Method

BRRRR stands for buy, repair, rent, refinance, and repeat. Information technology is a corking style to get into rentals with less money down. You will need to become an awesome bargain to make this strategy work, just you may be able to go all of your money back. Y'all purchase a house that is an amazing deal, ready it upward, rent the property, and then refinance information technology. One time the refinance is done you repeat over and over! The central to making this strategy work is getting an awesome deal with plenty of equity. You also demand to exist prepared if things practise not go perfectly. Appraisals tin come in depression, the banks may not want to finance you, yous may non get the belongings rented or repaired every bit fast as hoped, etc.

Hard money loans

Using hard money can salve you a ton of greenbacks in the short-term, but information technology is more expensive in the end. Fannie Mae lending guidelines, let you to refinance a home with no seasoning period, which ways y'all do not have to wait half dozen months or a year later you purchase a domicile, to refinance at a higher value than what you bought information technology for. Fannie Mae guidelines base the refinance amount on a new appraisement, and they volition allow a 75 percent loan-to-value ratio. Fannie Mae guidelines practice not allow a cash-out refinance, simply they do allow the refinance to pay off any existing loans. Many hard money lenders will permit a buyer to borrow up to 100 percent of the buy toll and to finance repairs as well.

Since Fannie Mae guidelines let a 75 percent loan-to-value refinance, theoretically an investor could buy a habitation for $100,000 and get a loan with a hard money lender for $100,000 plus $30,000 in repairs for a total loan amount of $130,000. The investor could refinance the home for equally much as 75 percent of a new appraisal. If the appraisement came in at $180,000, and then 75 percent loan-to-value would let a refinance of $135,000. Fannie volition not permit a cash-out refinance, only the investor could refinance the full $130,000 loan amount. This strategy can be costly due to hard money fees, but it allows the investor to refinance the entire buy price and repairs!

This strategy can also be very risky because you are depending on a high appraisal to get your money out. Most hard money loans are merely one year and you must pay off the loan after that year. Refinance appraisals are not always as high equally we would like them to exist. Brand sure you take an exit strategy if the appraisal comes in lower than you expect.

Private money loans

I legitimate way to buy real estate with no money down is to utilise private money. Individual money is from a private investor, friend, or family member. The individual investor will give yous money at a certain interest rate to buy a flip or rental property. Private money rates tin vary from very cheap to very expensive depending on the relationship, investment, and terms of the loan. I use private money from my sister for my fix and flips. She charges me six pct interest. Information technology is a cracking manner to reduce the amount of cash I have into the properties.

I have used individual money to buy commercial rentals and and then refinance into a long-term loan with a local banking concern.

Can being a existent estate agent help?

At that place are many advantages to having your existent manor license, but the biggest do good is you can proceed your commission on virtually every house you buy. On a $100,000 firm, your commission could be $iii,000 dollars or more than. Hither is an article that details why it is an advantage to become a real estate agent if you are an investor. Existence a real estate amanuensis as well gives me an reward in finding and purchasing peachy deals. I detail how difficult it is to get your real estate license here. I saved more than $270,000 a year on commissions by being a real estate amanuensis. That does not include the money I made on deals that I got considering I was an agent.

Turnkey rentals

A new trend in the US is buying turnkey rental properties that are purchased, repaired, rented, and managed by a turnkey provider. Turnkey properties are a great opportunity for investors to buy rental properties out-of-state when homes are too expensive in their area. At that place are turnkey providers who offer as little equally v per centum downward for investors, but they tend to have very high-interest rates. Here is a slap-up article nigh turnkey providers or transport me a request here for turnkey providers I know of. I bought a turnkey rental in Cleveland a few years agone.

Line of credit

I have had many lines of credit in my career. I have had lines of credit against my personal house (the house I live in) and my investment properties. Information technology is much easier to become a line of credit against your personal firm and some banks will not even offering lines of credit on investment properties. A line of credit is basically a loan against a home, but yous do not accept to utilise the money all the time. If you practice non demand the money y'all can pay it back to the banking company and not exist charged interest on it. When you need the money once more, you can borrow it very quickly as long equally the line is open.

Off-market properties

Off-market properties are purchased through direct marketing or by word of mouth. Ownership off-marketplace usually ways less expensive backdrop and in some cases, owners with flexible terms such as owner financing. Many investors wholesale off-market properties, which you can purchase with no down payment. Wholesaling is a process of ownership and selling properties very rapidly. The properties must be very expert deals and are usually found past direct marketing for properties. Many investors brand a great living by only wholesaling properties to other investors.

Seller financing

Some sellers may be willing to finance the house they are selling or finance a 2nd loan on a home that allows a buyer to put less than 20 percent down. If your bank is willing to offer fourscore per centum loan-to-value, the seller may offer to loan the other 20 percent, which would amount to no coin down for the buyer. The seller may also offering a number of other loan-to-value percentages to help a buyer get into a home for less than 20 percentage downward.

Finding seller-financed properties is the tricky role. Most sellers are not looking to finance a loan when they sell. To find seller financed listings, look for homes that have no loans against them or an MLS listing description that say seller financing is available. The seller's terms can vary greatly depending on how drastic they are to sell and what exactly they are looking to exit of the deal. Exercise not expect to pay 4 percent interest on a seller-financed loan; they will want a premium on whatever money they lend. It is also harder to find great deals with seller financing, which is fundamental to my strategy.

In that location are many new restrictions on financing thanks to the recent Dodd-Frank Human activity.

Refinance

In almost areas of the country, dwelling values are rising and involvement rates are at record lows. You may be able to refinance your home and get enough money to buy an investment property. Once you are able to purchase an investment property, you can refinance it in one year (sometimes less with the right banking company). With rates as low equally they are, if you lot bought the dwelling house below market value, you should be able to accept out equally much as you put into the house and still cash flow. I utilise this refinance technique all the time. Getting lenders to exercise a refinance is tricky when you lot own multiple investment properties. I apply a portfolio lender who has allowed me to utilize a greenbacks-out refinance on equally many backdrop as I want.

Below is a holding I refinanced:

Motility in ready Houses

A move-in ready property ways all the repairs are completed and it is set to hire every bit soon every bit you buy the habitation. There tin can exist many advantages to ownership a nice domicile. The biggest advantage is you practice not accept to pay for repairs. You too do not have to spend time waiting for repairs to exist done, which saves money on mortgage payments, utilities, and other carrying costs. The downside of a motion-in ready property is that information technology is usually more expensive and provides less greenbacks menstruation than a dwelling house that needs work.

Credit cards

A few other ways to go quick cash can exist very expensive and are commonly reserved for people looking to do a quick flip. If you have a killer deal you cannot turn down, you may want to consider these options, but I do not recommend using them unless it is necessary. The easiest way to go quick cash is with credit cards. You can get a cash accelerate or pay for repairs using your credit card. If y'all use a credit card to finance your downwardly payment or repairs and cannot pay it off right away, do not pay the 17 per centum interest charge per unit. Practice your best to get another card that will allow a balance transfer. Many times, you lot can transfer all of your residue and pay little to no interest for up to a year. That may give you enough time to pay off the card and not to be stuck with a high-involvement charge per unit eating all of your profits. I also propose using a rewards menu for repairs on your investment properties. If you pay the residuum off every month, this is a great way to make a little extra money.

Self-directed IRA

If you have money invested in an IRA, you are non limited to investing in stocks or mutual funds. At that place are special cocky-directed IRAs that you lot can use to purchase an investment property. You tin employ your IRA for down payments and repairs and then collect rent in the IRA.

401K

Some 401ks permit an investor to take out a loan against them. Yous usually have to pay back the loan relatively quickly and pay interest on the loan. You have to be very careful when borrowing from a 401k because the money yous borrow is no longer earning interest or growing in your retirement fund. If you lose your job, you also may exist required to pay back the loan inside 60 days or pay a 10 per centum penalty and income tax on the loan.

Subject to loans

With a bailiwick to loan, you lot buy a house without paying off the previous owner's mortgage. This is another tricky situation; investors must be very conscientious with it. Most banking company mortgages are not assumable; when the homeowner sells the house, they have to pay the loan in full. The bank almost likely will accept a due-on-sale clause that says the loans must be paid in total, one time the holding transfers ownership. With subject to loans the new investor buys a house subject to an old mortgage and does non pay off the loan. There is a chance that the bank will require the loan to be paid off if they find out that the home has been sold.

Investors buy homes subject to a mortgage then that they do not have to get a new loan. It may exist hard for the investor to authorize for a mortgage or they may be maxed out on being able to get new loans. If y'all buy a habitation for $80,000 that has a $75,000 mortgage in place, the investor would simply need $5,000 to purchase the house instead of the normal 20 percent or more.

Fannie Mae Homepath program

The Fannie Mae Homepath program on their REO properties allows investors to put only 10 per centum down and allows up to 20 financed loans in one person's name, which is too a huge bonus. Information technology is very difficult for many investors to get loans on more than than four backdrop.

This programme has been discontinued.

Conclusion

Rental properties tin be expensive, just there are ways to purchase them with less than 20 percent downward. If y'all are brusk on cash, buying properties with picayune money down can accelerate the purchasing schedule and increase your returns. However, y'all will most probable brand less money on each belongings, because borrowing that concluding twenty percent can be much more expensive than the first 80 percent.

My book Build a Rental Property Empire, goes over how to buy investment properties with lilliputian coin down. It also covers how to find deals, finance rentals, manage them, and much more! It is available as a paperback and ebook on Amazon or as an audiobook on Audible.

Source: https://investfourmore.com/investment-property-no-money-down/

Posted by: mendezloomely.blogspot.com

0 Response to "How To Register Rental Property With State Of Maine"

Post a Comment